American workers of all generations put comfortable retirement among their top life goals, yet a large percentage are uncertain about how to plan for it, when to retire, and how they will pay for it, according to the latest Retirement Security Survey released today by retirement and investment leader Principal Financial Group®.

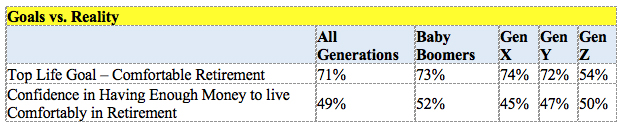

In a national survey of those with workplace retirement plans held by Principal®, 71% listed “living comfortably in retirement” as a top life goal along with good health and financial wellness. Unfortunately, less than half (49%) have confidence that their savings will be enough, and a further 55% don’t feel secure in their retirement planning.

“Time and again, Americans overwhelmingly say they want a comfortable retirement, and shifts in the past few years about how we work and think about work has not changed that,” said Sri Reddy, senior vice president, Retirement & Income Solutions at Principal. “But our research shows there is a lot of work to be done to help people feel more secure and confident in their planning. It’s our job to demonstrate how the right tools, resources, and education can help people remain calm through bouts of market volatility while still preparing for the future.”

The latest research gathers insights from workers, retirees, and plan sponsors about their experiences and views related to retirement planning and financial well-being. The findings reveal a wide, but not insurmountable gap between retirement saving goals and confidence levels in reaching the best outcomes. Key findings include:

Knowledge and retirement plan capabilities are key to boosting confidence. Fifty percent of workers of all generations are either unsure how much they should be saving for retirement, or know they are saving less than they should be to reach their goals. Workers see the top criteria for reaching retirement goals as: employer match-contributions (62%), a balanced investment portfolio (52%), and financial advice and guidance (51%).

Lack of confidence may be due to the changing nature of retirement. Historically, retirement timing in America was primarily driven by the age a person could collect Social Security and pension or defined benefit plan payments. Today, workers cite “when I’ve saved enough” or “when I cannot do the work any longer” as determining factors for retirement. Meanwhile, only 47% of workers are confident they have the knowledge to make good decisions with their retirement account ahead of a job change or retirement. That confidence level has dropped from 59% in Q1 2021.

Having a steady paycheck in retirement beyond Social Security is an elusive goal. The majority of workers lack confidence that Social Security will be available to them, with 64% citing it’s viability for them as a concern, including a whopping 73% of Gen Z workers. That said, only 30% created their retirement savings goal based on an estimated “income floor” in retirement (or what they need to cover monthly essential expenses), and 73% admit they lack knowledge of how to create income from savings.

“In a world where fewer Americans have pensions, securing a source of steady income beyond Social Security is not only smart, but can provide confidence for people to spend the money they’ve worked so hard to save without fear of running out,” Reddy said. “Identifying an ‘income floor’ in retirement is a great way for people to kickstart this process.”

On the plus side, the Principal survey of plan sponsors shows employer awareness of the need for stronger retirement plans and benefits. Findings include:

Employers, many in search of talent, are poised to bolster retirement planning and benefits. Just 39% of plan sponsors feel their employees are doing a good job preparing for retirement and a mere 15% feel their employees will have enough money saved. That said, they know offering a retirement plan is important for maintaining their workforce, with about half citing retention and attraction as a top reason to offer a plan, and 61% feeling it’s important for employees to participate.

Employers know there’s opportunity to do more. Over two-thirds (68%) of plan sponsors feel responsible for making a retirement plan available to employees. But 32% say they don’t do enough to encourage employees to increase their deferral savings percentage, and 33% feel they don’t do enough to encourage employees to start planning for income in retirement—two key areas for improvement.

To learn more about how workers, retirees, and plan sponsors are navigating retirement security today, visit Principal at this link.