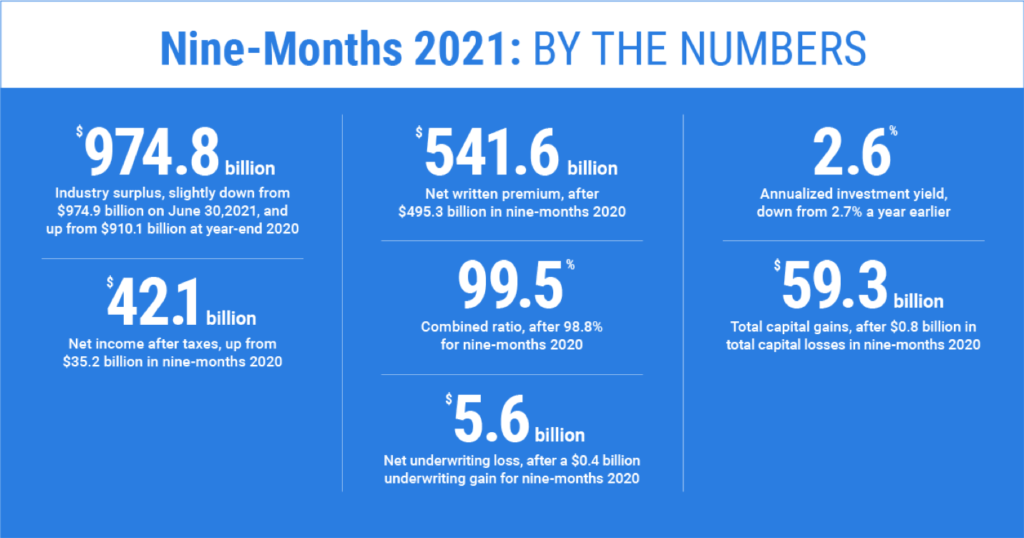

Private U.S. property/casualty insurers saw a $5.6 billion net underwriting loss in the first nine months of 2021, as non-catastrophe losses returned to pre-pandemic levels, according to a report by Verisk (Nasdaq:VRSK), a leading global data analytics provider, and the American Property Casualty Insurance Association (APCIA).

Direct losses for personal auto liability increased 14.1% in nine months 2021 and the industry’s combined ratio—a critical measure of insurer profitability—worsened to 99.5%, from 98.8% a year earlier. While non-catastrophic losses were on the rise, insured catastrophe-related losses remained high. Both in 2020 and 2021, estimated nine-months net loss and loss adjustment expenses from catastrophes exceeded $48 billion.

Despite the underwriting loss, the industry saw an increase in net income after taxes to $42.1 billion in nine months 2021, from $35.2 billion a year earlier. This increase was fueled in part by premium growth and investment gains. Insurers’ overall profitability—as measured by their annualized rate of return on average policyholders’ surplus—rose to 6.0% in nine months 2021 from 5.5% a year earlier.

Overall net written premium growth accelerated to 9.4% in nine months 2021, from 2.9% the year prior, as the economy was on the path for recovery from the massive disruptions caused by COVID-19 in 2020.

“While catastrophes, including hurricane Ida in September 2021, brought major insured losses, it was an increase in non-catastrophic losses, especially in personal auto, that contributed the most to the worsening of underwriting results in 2021,” said Neil Spector, president of underwriting solutions at Verisk. “As the economy continued to recover, insurers saw incurred losses return to more typical levels, additionally pushed up by inflation and supply chain issues. Going into 2022, the insurance industry continues to face a wide range of challenges, from climate change to evolving cyber threats. Those insurers with access to robust data from across the industry will be the best equipped for the constantly changing risk landscape.”

“Insurers are facing an extreme escalation in inflationary pressures that increasingly strained rate adequacy last year,” said Robert Gordon, senior vice president policy, research, and international, for the American Property Casualty Insurance Association (APCIA). “While both net written and net earned premiums increased during the third quarter, incurred losses and loss adjustment expenses increased even more (by 17.8%). Net underwriting losses worsened in the third quarter, driving insurers’ combined ratio to 104.5 and contributing to a 57% plunge in net income after taxes. Hurricane Ida contributed to continuing severe levels of catastrophe losses while increased auto accident frequency and severity spiked auto loss ratios.”

2021’s Third Quarter Sees Elevated Loss Levels

In third quarter 2021, insurers saw their net income after taxes decline to $4.7 billion from $10.9 billion the year prior. The industry’s operating income was $2.5 billion, down from $7.7 billion in third quarter 2020.

Loss and loss adjustment expenses increased in third quarter 2021 to $143.1 billion from $121.4 billion a year earlier. These helped drive the loss ratio for the quarter to 79.3%, the highest quarterly loss ratio since third-quarter 2017, when Hurricanes Harvey, Irma and Maria caused extensive losses.

The combined ratio deteriorated to 104.5% in third quarter 2021 from 101.3% in third quarter 2020.

Read the full report from Verisk and APCIA.